Investors have rewarded the entire SaaS industry to pursue growth over profitability for a long time. But TSIA believes those days are waning.

There are new expectations for what defines a highly valuable SaaS business.

As we enter 2023, the SaaS (software-as-a-service) business model has been with us for over twenty years. Traditional software companies like Adobe, Autodesk, and Microsoft have pivoted to SaaS. But just as everyone is jumping on the SaaS bandwagon, current economic conditions are forcing high-growth (but unprofitable) SaaS startups to tighten their financial belts.

In this blog, we’ll answer the question, “why are SaaS companies unprofitable?” by explaining:

- The new normal for SaaS companies

- Factors inhibiting profitability:

- Why you can’t cut your way to success

The New Normal

In September of 2022, Salesforce, the poster child for growth over profitability, committed to improving their operating margin by five percentage points—which is massive.1 But keep in mind, this is a company with roughly $30 billion in annual revenues that still struggles to post a positive net operating income.2 Salesforce, just like many other SaaS companies, will be operating in the new normal.

There are three economic realities that are forcing SaaS companies to focus on profitability as we enter 2023:

- Inflation

- Higher interest rates

- Depressed company valuations

Unfortunately, there is no sign that these three realities will be changing in the coming year. In addition, a significant recession may be a fourth factor that comes into play in 2023. The cost of employees and infrastructure is increasing. Borrowing money to cover costs is becoming more expensive—and you can’t leverage a soaring company valuation.

In this new normal, SaaS companies will have to focus on improving free cash flow and overall profitability.

For over a decade, TSIA has been studying the difference between profitable and unprofitable SaaS business models. There are three main factors that are inhibiting the ability for a majority of SaaS companies to become profitable:

- Blunt economic engines

- Subsidized costs

- High RAC (revenue acquisition costs)

The Blunt Economic Engines of Unprofitable SaaS Companies

Before we analyze the economic engines of unprofitable SaaS companies, we need to review how enterprise software companies have historically been so profitable. In the world of on-premise, licensed software, there are three critical revenue streams:

- License Revenue: When the customer pays for the right to own and use a copy of the software or hardware product.

- Annuity Services: When the customer pays for ongoing support or premium support. Usually in an annual or multi year contract.

- Project Services: When the customer pays the software provider for specific deliverables such as software implementation or technical training. These services may be a fixed-fee or charged on a time-and-materials basis.

Over the decades, software companies migrated to one of two common economic engines related to these three revenue streams:

- Product Providers: Companies that receive a majority of their revenue from the act of selling the license.They defer much of the annuity and project service revenues to a partner ecosystem.

- Product Extenders: Companies that receive the largest source of revenue for maintenance. These companies also have a 10% to 20% of revenue coming from project-based services.

The revenue mix for these two profiles is shown in Figure 1.

Figure 1: Revenue Mix of License-Based Software Companies (Expand image) The margin profile for these three revenue streams has been very favorable:

- Product: Software license margins are typically reported with gross margins above 90%.

- Annuity Services: TSIA does extensive benchmarking in the area of software maintenance. Margins for this business comfortably run in the 70% to 86% range.

- Project Services: TSIA also conducts extensive benchmarking related to this service line. Project-based services for product companies are the lowest gross margin activity in the economic engine. Yet, these services are still experiencing an average gross margin in the mid 30s, with best-in-class performers achieving gross margins in the high 40s.

These two profiles, when well executed, have proven to be highly profitable. Well-managed, publicly-traded, license-based software companies have generated anywhere from 12% to 47% in net operating revenue.

Now, let's turn to the economic engine of SaaS companies and answer the question…

Why Are SaaS Companies Unprofitable?

SaaS companies don’t charge a customer for a license or a maintenance contract. SaaS customers purchase a subscription that gives them access to a software platform and any future enhancements that may occur on that platform. This means the revenue streams experienced by SaaS companies are slightly different:

- Subscription Revenue: When the customer pays for access to the software platform.

- Annuity Services: When the customer pays for ongoing premium support or services, usually in an annual or multi year contract.

- Project Services: When the customer pays the software provider for specific deliverables such as migration or technical training. These services may be fixed-fee or charged on a time-and-materials basis.

To date, a majority of SaaS providers have gravitated to one economic engine that is dominated by subscription revenues.

SaaS companies will often only have 5% to 10% of revenues coming from any type of additional services. These services are a blend of project and annuity offerings. However, it is very common for SaaS companies to run these services at a financial loss. The revenue mix of a typical SaaS provider is shown in Figure 2.

Figure 2: SaaS Economic Engine (Expand image) The margin profile for these three revenue streams have not proven as lucrative when compared to what we have seen in the traditional software models:

- Subscription: In the TSIA Cloud 40, average subscription margins are running 68%. In the seven years we have been tracking the index, his number has not budged.

- Annuity Services: Many SaaS providers lump annuity services and project services together in one bucket that is reported as “services.” In the last TSIA Cloud 40 snapshot, the average gross margin for this services bucket was 66%. However, TSIA does benchmark SaaS providers. When looking specifically at premium based annuity services, TSIA is seeing SaaS providers achieve gross margins in the 80%-plus range.

- Project Services: In the TSIA Cloud 40, the few companies that break out the margins on their project services report an average gross margin of -9%—well below the project margins achieved by traditional software companies. TSIA has benchmarked the professional services businesses of many SaaS providers, and we are seeing a bifurcation in the performance of this revenue stream. Some SaaS companies are running professional services at a loss, and there is evidence of this in the public record. Other SaaS companies are running professional services for a profit, achieving gross margins that are actually higher than what we see with traditional software companies—project margins that are north of 40%.

Overall, this economic engine has not proven to be very profitable.

Publicly-traded SaaS companies tracked in the TSIA Cloud 40 Index are currently generating an average of -10.6% operating income.

Figure 3 provides evidence of how consistently poor the average operating income has been for these companies.

Figure 3: Average Operating Income, TSIA Cloud 40 (Expand image)

Now, the argument is often made that these SaaS companies are relatively small. When they put on weight, they will become highly profitable like traditional software companies. Sadly, that is not the case. Figure 4 compares SaaS companies with revenues over $500 million to the performance of traditional software companies in the same quarter.

Figure 4: Large Saas Companies versus Traditional Software Companies (Expand image) The bottom line: The largest SaaS companies in the world are generating operating incomes equivalent to low-margin retailers.

Subsidized Costs

There are four cost factors that depress the profitability of SaaS companies:

- Infrastructure: By definition, SaaS companies are providing the software as a service. This means the customer does not have to purchase hardware to run the software—that cost is transferred to the SaaS provider. This cost bucket is not going away, as it comes with being a SaaS provider. However, with inflation, the costs in this bucket are (painfully) increasing.

- Technical Support: In the traditional software model, companies learned how to effectively monetize technical support. For companies like Oracle, SAP, and a host of other enterprise software companies, maintenance and technical support contracts became the largest gear in the economic engine. A majority of SaaS companies roll all of the costs associated with technical support into the cost of the subscription.

- Professional Services: As already highlighted, many SaaS providers are providing professional services capabilities for free or at a financial loss. To date, the rationale has been to make it easy for customers to get up and running by not attempting to effectively monetize these services.

- Customer Success: Finally, TSIA benchmarks show that only half of companies we benchmark monetize any customer success motions. This means SaaS providers are covering the cost of customer success in either sales and marketing expenses or subscription cost of goods sold (COGS).

Again, infrastructure costs are not going away. But the practice of simply eating all of the costs of technical support, professional services, and customer success are contributing to lower operating margins and high sales and marketing expenses as documented in Figure 5 below.

Figure 5: TSIA Cloud 40 Financial Model

High Revenue Acquisition Costs (RAC)

As shown, SaaS companies spend the largest portion of their revenue on sales and marketing expenses—twice as much as they do on research and development (R&D). Historically, this was never viewed as problematic because that high investment in demand generation was justified by high growth rates. This thinking is what gave birth to the infamous “Rule of 40.”

What is the Rule of 40? And how do you calculate it?

The Rule of 40 is designed to reward growth. The rule permits management teams to sacrifice profitability for growth—within reason. According to this rule, a business' combined growth rate and operating margin should be over 40%.

Rule of 40: Annual Growth Rate + Operating Margin >= 40%

However, companies in the TSIA Cloud 40 are spending, on average, 39% of revenue on sales and marketing to grow at 24% and achieve a -13% operating income. In other words, on average, they are “Rule of 11” companies, which is nowhere near the objectives of the Rule of 40.

Companies that spend a high percentage of revenue on sales and marketing but are not growing at a rate to justify that high spend will not be Rule of 40 companies.

One way to assess the efficacy of sales and marketing efforts is to measure customer acquisition costs (CAC). CAC is the cost related to acquiring a new customer.

In other words, CAC refers to the resources and costs incurred to acquire an additional customer. Customer acquisition cost is a key business metric—unfortunately, TSIA knows it is a minority practice for companies to accurately track and trend CAC. But, we can use a simple proxy for CAC which TSIA is defining as revenue acquisition costs (RAC):

RAC = Annual % of Revenue Spent on Sales and Marketing / Annual Revenue Growth Rate

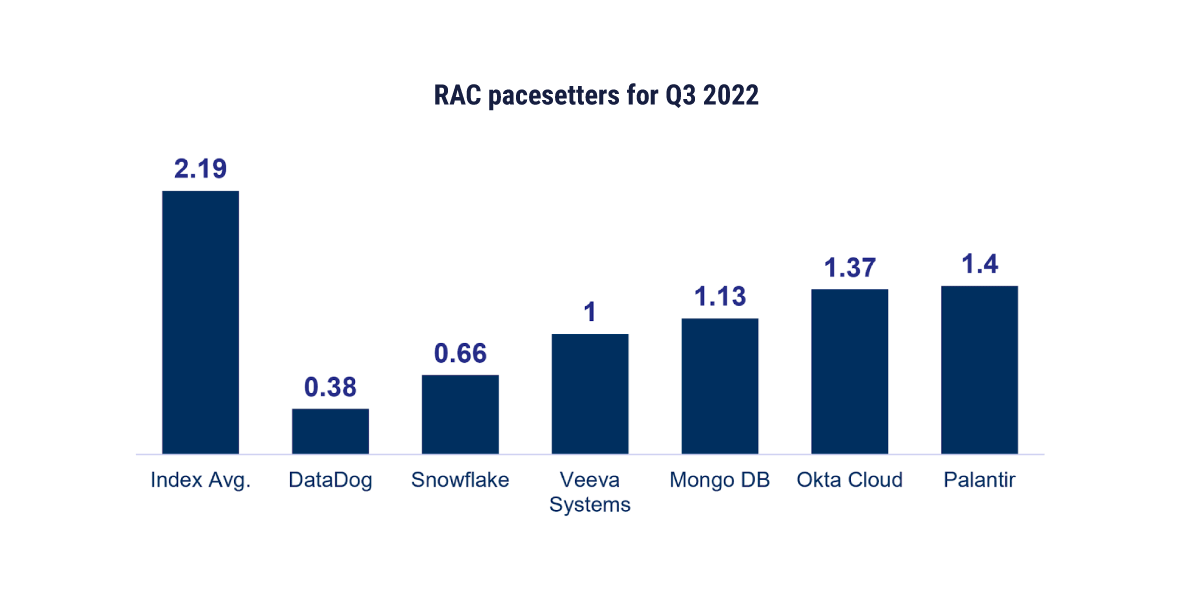

In Q3 2022, The average RAC number for companies in the Cloud 40 Index was 2.19. This means that for every 1% of topline growth, these companies spent 2.19% of total revenue.

TSIA would assert that companies paying more for growth than their technology industry peers are inefficient compared to their peers. The lower RAC number a company achieves, the more efficiently the company is growing revenues. Two levers can reduce RAC:

- Increasing the growth rate of revenues and keeping the percentage of revenue spent on sales and marketing the same (or lower).

- Reducing the percentage of revenue spent on sales and marketing and keeping the revenue growth rate the same (or higher).

Every quarter, TSIA captures the RAC rating for companies in the T&S 50 and the TSIA Cloud 40. Companies can use this rating to assess how efficiently they are generating revenue compared to relevant industry peers. Figure 6 provides a snapshot of RAC pacesetters for Q3 2022.

FIGURE 6: RAC Pacesetters Q3 2022

You Can’t Cut Your Way to Success

Based on the analysis so far, it is clear that unprofitable SaaS companies are facing a dilemma. They are carrying costs for infrastructure and service motions that highly profitable legacy software companies never had to bear. And, the cost of acquiring revenue growth is proving very high.

The intuition of management teams will be to cut costs to achieve improved probability. For SaaS companies that have been enjoying cheap funding and free-flowing spending, there is clearly an opportunity to tighten their belts. However, TSIA does not believe cutting spending in the current SaaS business model will rightsize profitability. Here is why.

Again, the largest expense category for SaaS providers is sales and marketing. So let's start there. The largest expense within sales and marketing are sales reps. Since the growth of most SaaS companies is heavily dependent on direct sales motions, executive teams are highly reluctant to cut here.

So, what else is in this bucket? Perhaps some of the customer success motions are funded here. These CSMs may not be carrying any direct revenue responsibilities, so this seems like a good place to start cutting. But CSMs are there to drive adoption which leads to the expansion and renewal of contracts. The highest margin revenue for any SaaS provider comes from existing customers. Putting that revenue in jeopardy is risky.

The second largest cost category is subscription COGS. The majority of this expense is for the infrastructure required to support the offer. You can look for inefficiencies here but it is unlikely you can make meaningful cuts. The remaining expense is for technical support motions that are included with the subscription.

It will be VERY tempting to reduce funding for support, but this carries the same risk as cutting customer success function. Customers that cannot technically access the solution surely are not adopting and eventually will not renew.

To Become Profitable…

Are there expenses that SaaS companies can trim? Absolutely.

But to become profitable, on average, SaaS companies need to find 11 points of cost savings! You don’t take that number down by trimming across the board and then handicapping key capabilities.

The good news is that TSIA has a perspective on how SaaS companies can escape this profitability conundrum. To be part of this ongoing conversation, join the TSIA community—become a member today.

1 Dan Gallagher, "Salesforce Not Slacking on Margin Focus," Wall Street Journal, Sept. 2022.

2 Salesforce, Inc. (2022). Form 10-Q. U.S. Securities and Exchange Commission.

Growth versus Profitability Shouldn't Be a Choice

Want to assess your efficiency and profitability? In this report, learn more about the Rule of 40 and RAC.

Want help navigating the growth versus profitability conundrum? TSIA helps you achieve profitable growth at a fraction of traditional consulting costs. Contact us to learn more.

About Author Thomas Lah

Thomas Lah is executive director and executive vice president of TSIA. Since 1996, he has used his incisive analysis, strategic thinking, and creative solutions to help some of the world’s largest technology companies improve the efficiency of their daily operations. He has authored several books, including, Bridging the Services Chasm (2009), Consumption Economics (2011), B4B (2013), and Technology-as-a-Service Playbook: How to Grow a Profitable Subscription Business (2016), and Digital Hesitation: Why B2B Companies Aren’t Reaching Their Full Digital Potential (2022). He is also the host of TSIA’s podcast, TECHtonic: Trends in Technology and Services.

Smart Tip: Embrace Data-Driven Decision Making

Making smart, informed decisions is more crucial than ever. Leveraging TSIA’s in-depth insights and data-driven frameworks can help you navigate industry shifts confidently. Remember, in a world driven by artificial intelligence and digital transformation, the key to sustained success lies in making strategic decisions informed by reliable data, ensuring your role as a leader in your industry.